Tax Alert July (3) 2018

23 Jul 2018Sales Tax and Service Tax

The long-awaited Sales Tax and Service Tax (“SST”) frameworks have finally been released by the Royal Malaysian Customs Department (“RMCD”) on 19 July 2018. The effective date of the SST implementation will be on 1 September 2018. The proposed Sales Tax and Service Tax implementation models and Frequently Asked Questions (“FAQ”) are downloadable at the RMCD’s website at the links below:

http://gst.customs.gov.my/en/hl/_layouts/CustomApplication/Announcements.aspx

http://www.customs.gov.my/ms/Pages/sst.aspx

The pertinent points announced are as follows:

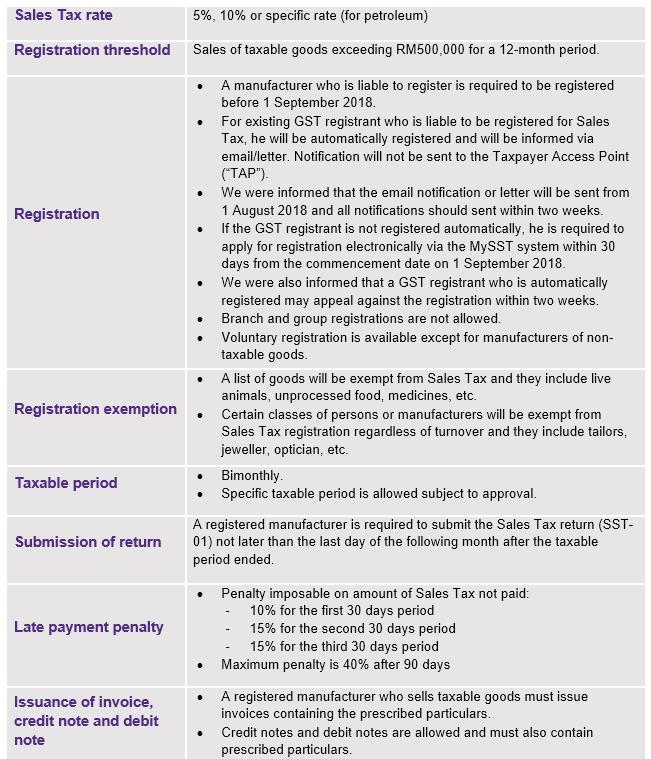

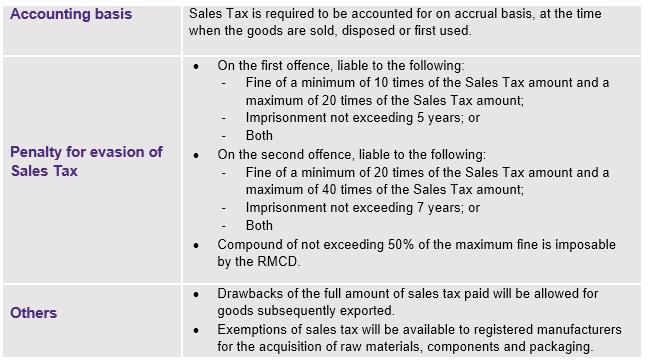

SALES TAX

Sales Tax is a single-stage tax charged and levied on taxable goods manufactured and sold in Malaysia by a taxable person as well as taxable goods imported into Malaysia. The activity constituting manufacturing will be defined.

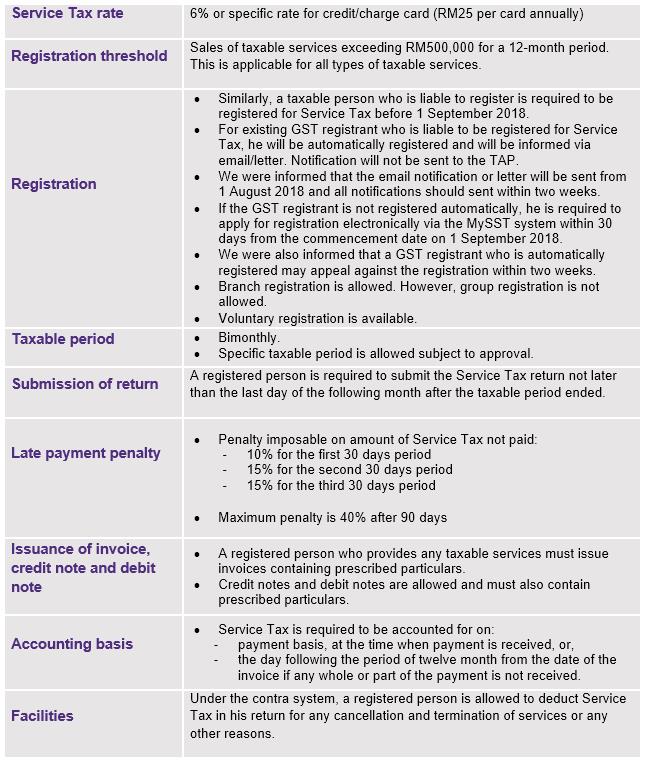

SERVICE TAX

Similarly, Service Tax is a single-stage tax. Service tax is charged on the provision of taxable services made in the course or furtherance of any business by a taxable person in Malaysia.

Service Tax is not applicable to imported services and exported services.

Impact on GST

- There are guidance provided for the transition from GST to SST.

- Input tax from the GST era is claimable within 120 days after the effective date of SST.

- Deregistration of GST is not required. A GST registered person will automatically ceased to be a GST registered person when the Goods and Services Tax Act 2014 is repealed.

- A GST registered person is required to account for output tax at the standard rate of 0% for goods held on hand before the effective date of SST.

- Audits for closure of GST will still be carried out after 1 September 2018.

Please do not hesitate to contact us should you wish to discuss any matters relating to SST or GST.