Our ‘Insights into MFRS 15’ series summarises the key areas of the Standard, highlighting some areas that are challenging to apply in practice, to assist reporting entities in understanding how to apply MFRS 15’s requirements. This article focuses on the objective and scope of MFRS 15.

Overview: A single model for revenue recognition

MFRS 15 is based on a core principle that requires an entity to recognise revenue:

- in a manner that depicts the transfer of goods or services to a customer, and

- at an amount that reflects the consideration the entity expects to be entitled to in exchange for those goods or services.

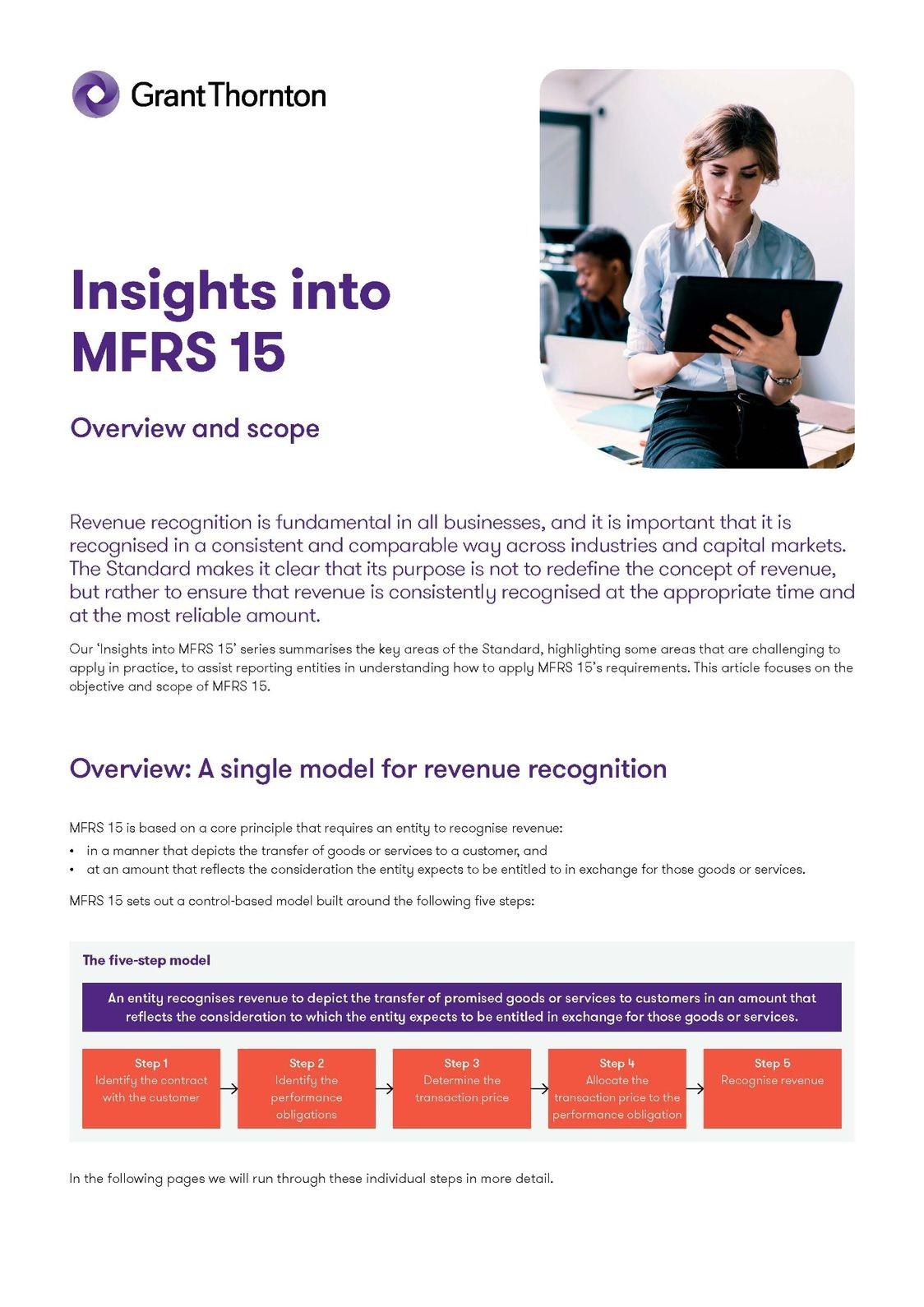

MFRS 15 sets out a control-based model built around the following five steps:

The five-step model

An entity recognises revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

- Step 1 - Identify the contract with the customer

- Step 2 - Identify the performance obligations

- Step 3 - Determine the transaction price

- Step 4 - Allocate the transaction price to the performance obligation

- Step 5 - Recognise revenue

Insights into MFRS 15 Overview and scope

Read our publication to understand the objective and scope of MFRS 15.

How we can help

We hope you find the information in this article helpful in giving you insight into aspects of MFRS 15. If you would like to discuss any of the points raised, please speak to your usual Grant Thornton contact.