Introduction: Why accounting estimates matter in modern financial reporting

Financial statements are intended to present a true and fair view of an organisation’s financial position and performance. However, not all financial information can be measured with precision. In many areas of accounting, uncertainty is unavoidable, and management is required to apply judgement when determining values. This is where accounting estimates play a critical role.

Accounting estimates are integral to financial reporting across all industries. They affect key balances such as asset valuations, provisions, impairments, and revenue recognition.

For CFOs, directors, and those charged with governance, understanding how accounting estimates are developed, applied, and reviewed is essential. This is essential, not only for accurate reporting, but also for maintaining credibility with stakeholders and auditors during a financial statement audit.

As business environments become more complex and volatile, the significance of accounting estimates continues to increase. This places greater emphasis on governance, documentation, and transparency around how estimates are determined.

What are accounting estimates?

Accounting estimates are approximations of monetary amounts used in financial statements when precise measurement is not possible. They arise due to inherent uncertainties in business activities, future events, or valuation inputs.

Unlike accounting policies, which define how transactions are recognised and measured, accounting estimates determine the amounts recognised based on the available information at the reporting date.

Common characteristics of accounting estimates include:

- Reliance on assumptions about future outcomes

- Use of historical data combined with forward-looking information

- Application of management judgement

- Susceptibility to change as new information becomes available

Accounting standards acknowledge that estimates are an unavoidable and legitimate aspect of financial reporting, provided they are made on a reasonable and supportable basis.

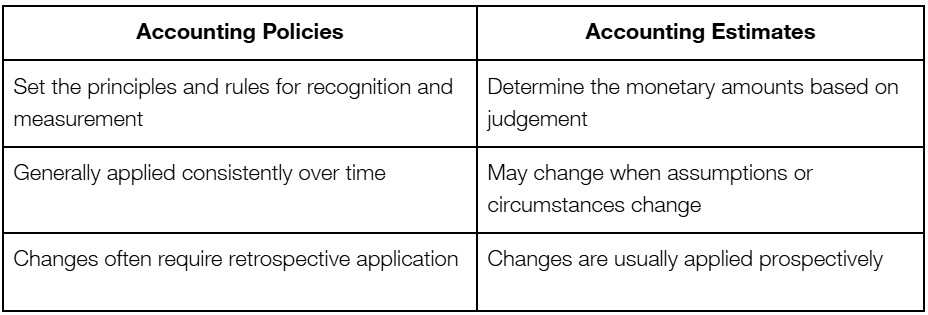

Accounting estimates versus accounting policies

A clear distinction between accounting estimates and accounting policies is essential for accurate reporting and disclosure.

For example, selecting the straight-line method of depreciation is an accounting policy, whereas determining the useful life of an asset is an accounting estimate.

This distinction is important because changes in accounting estimates are treated differently from changes in accounting policies under financial reporting standards.

Common examples of accounting estimates in financial statements

Accounting estimates appear throughout the financial statements and affect both profit or loss and the statement of financial position. Common examples include:

1. Allowance for doubtful debts (expected credit losses)

Management must estimate the portion of trade receivables that may not be recoverable. This involves assessing customer credit risk, historical default patterns, current economic conditions, and forward-looking factors.

2. Inventory obsolescence and net realisable value

Estimating inventory write-downs requires judgement about future demand, selling prices, and the condition or age of inventory items.

3. Depreciation and amortisation

Useful lives, residual values, and consumption patterns of assets are estimates that significantly affect depreciation and amortisation expense.

4. Impairment of assets

Impairment testing involves estimating recoverable amounts using value-in-use or fair value models, often relying on cash flow projections and discount rates.

5. Provisions and contingencies

Estimating provisions for legal claims, warranties, or restructuring costs requires judgement about the likelihood and magnitude of future outflows.

6. Fair value measurements

Where assets or liabilities are measured at fair value, estimates may involve valuation models, market assumptions, and unobservable inputs.

7. Deferred tax assets

Deferred tax assets arise from temporary differences, unused tax losses, or tax credits. Recognising these assets requires management to estimate the likelihood of sufficient future taxable profits against which the deferred tax assets can be utilised. This involves judgement about future profitability, business forecasts, and tax planning strategies. Changes in assumptions or business conditions may significantly affect the amount recognised.

These estimates are often areas of heightened focus during a financial statement audit due to their subjectivity and potential impact on reported results.

Why accounting estimates require careful judgement

Accounting estimates are inherently uncertain because they are based on assumptions about future events that may not unfold as expected. This uncertainty increases during periods of economic volatility, regulatory change, or market disruption.

Key sources of estimation uncertainty include:

- Changes in economic conditions

- Volatility in markets or commodity prices

- Technological disruption or business model changes

- Regulatory or tax developments

- Shifts in customer behaviour or credit risk

As a result, estimates may need to be revised from period to period. Such changes do not necessarily indicate errors; rather, they reflect updated information and evolving circumstances.

For directors and audit committees, the challenge lies in ensuring that estimates are reasonable, unbiased, and appropriately disclosed, rather than optimistic or overly conservative.

Accounting estimates and the financial statement audit

From an audit perspective, accounting estimates are often classified as higher-risk areas due to their judgemental nature. Audit standards require auditors to devote specific attention to how estimates are developed and whether they are free from material misstatement.

During a financial statement audit, auditors typically assess:

- The appropriateness of the estimation methods used

- The reasonableness of key assumptions

- The consistency of estimates with external data and historical outcomes

- The adequacy of disclosures relating to estimation uncertainty

Audit firms in Malaysia apply risk-based audit methodologies that focus audit effort on estimates with the greatest potential impact on the financial statements.

Importantly, auditors do not replace management’s judgement with their own. Instead, they evaluate whether management’s estimates fall within a reasonable range based on available evidence.

Governance and accountability over accounting estimates

Strong governance over accounting estimates is essential, particularly for larger organisations and groups. Responsibility for estimates does not rest solely with the finance function; it extends to senior management and those charged with governance.

Good governance practices include:

- Clear documentation of estimation methodologies and assumptions

- Regular review and challenge of significant estimates

- Involvement of appropriate subject matter experts where necessary

- Transparent disclosure of key judgements and sensitivities

Audit committees play a critical role by overseeing how management develops significant estimates and how auditors evaluate them.

Disclosure of accounting estimates and judgement

Transparency is a key principle of high-quality financial reporting. Financial reporting standards require entities to disclose information that helps users understand the degree of judgement and uncertainty involved in accounting estimates.

Typical disclosures include:

- The nature of significant estimates

- Key assumptions and sources of estimation uncertainty

- Sensitivity to changes in assumptions

- Reasons for changes in estimates from prior periods

As financial reporting evolves, disclosure expectations continue to increase, particularly for estimates that have a material impact on reported performance or financial position.

Entities preparing for upcoming standards, such as MFRS 18, should also consider how enhanced presentation and disclosure requirements may affect the way accounting estimates are communicated to users.

Valuation and specialist input in accounting estimates

Some accounting estimates, particularly those involving fair value or impairment, require specialised valuation techniques. In such cases, management may rely on internal or external valuation expertise.

Areas commonly requiring specialist input include:

- Business valuations

- Financial instrument valuations

- Intangible asset valuations

- Complex impairment assessments

Robust financial reporting frameworks ensure that valuation assumptions are consistent with market data and aligned with applicable accounting standards.

Accounting estimates in a changing reporting landscape

Financial reporting is not static. Regulatory developments, standard-setting activity, and evolving stakeholder expectations continue to shape how estimates are prepared and disclosed.

Resources such as Malaysia’s MFRS hub provide guidance and updates to help organisations stay informed about technical developments that may affect accounting estimates and disclosures.

As reporting requirements evolve, organisations should periodically reassess whether their estimation processes remain appropriate and sufficiently robust.

Practical considerations for CFOs and directors

For senior leadership, accounting estimates should not be treated as a purely technical accounting exercise. They have real implications for:

- Financial performance and key metrics

- Investor and stakeholder confidence

- Audit outcomes and timelines

- Regulatory scrutiny

Practical steps to strengthen estimate quality include:

- Ensuring early identification of significant estimates

- Encouraging healthy challenge and professional scepticism

- Aligning estimates with business strategy and risk assessments

- Maintaining clear audit trails and documentation

These measures support smoother audits and more transparent financial reporting.

Conclusion: Accounting estimates as a cornerstone of credible financial reporting

Accounting estimates are an unavoidable and essential component of financial reporting. When applied thoughtfully and governed effectively, they enable financial statements to reflect economic reality despite uncertainty.

For CFOs, directors, and organisations operating in increasingly complex environments, understanding accounting estimates is critical as not only to meet reporting requirements, but also to support informed decision-making and maintain trust with stakeholders and auditors.

As scrutiny over judgement and transparency continues to increase, robust processes around accounting estimates will remain a cornerstone of high-quality financial reporting and successful financial statement audits.