-

Audit approach

Designing a tailored audit programme customised for your business, we will combine the collective skill and experience of assurance professionals around the world to deliver an audit that is efficient and provides assurance to your key stakeholders.

-

Audit methodology

We have adopted Grant Thornton International's Horizon audit approach and Voyager software, a revolutionary paperless audit designed to achieve a consistent standard of audit service.

-

MFRS

At Grant Thornton, our MFRS advisers can help you navigate the complexity of financial reporting.

-

Our local experts

Our local experts

-

Tax advisory & compliance

Our teams can prepare corporate tax files and ruling requests, support you with deferrals, accounting procedures and legitimate tax benefits.

-

Corporate & individual tax

Our teams can prepare corporate tax files and ruling requests, support you with deferrals, accounting procedures and legitimate tax benefits.

-

International tax & Global mobility services

Our teams have in-depth knowledge of the relationship between domestic and international tax laws.

-

Indirect tax

Our indirect tax specialists help clients in effective planning; assist to bring clarity to the legislation; assist and advise in audits or investigations. It is important for all entities, whether or not required to register for Sales Tax or Service Tax to analyse the impact of the taxes on their business operations, their revenues and expenses, and their customers and suppliers.

-

Tax audit & investigation

Tax audit and investigation

-

Transfer pricing

Transfer pricing

-

M&A, Restructuring & Forensics

Forensic

-

Corporate finance

Whether you are raising capital, disposing of a business or seeking a wider market for your company's shares on a stock market, we are ready to help make it a successful and stress-free experience for you.

-

Business risk services

We can help you identify, understand and manage potential risks to safeguard your business and comply with regulatory requirements.

-

Recovery and reorganisation

We provide a wide range of services to recovery and reorganisation professionals, companies and their stakeholders.

Tax Alert July (3) 2018

23 Jul 2018Sales Tax and Service Tax

The long-awaited Sales Tax and Service Tax (“SST”) frameworks have finally been released by the Royal Malaysian Customs Department (“RMCD”) on 19 July 2018. The effective date of the SST implementation will be on 1 September 2018. The proposed Sales Tax and Service Tax implementation models and Frequently Asked Questions (“FAQ”) are downloadable at the RMCD’s website at the links below:

http://gst.customs.gov.my/en/hl/_layouts/CustomApplication/Announcements.aspx

http://www.customs.gov.my/ms/Pages/sst.aspx

The pertinent points announced are as follows:

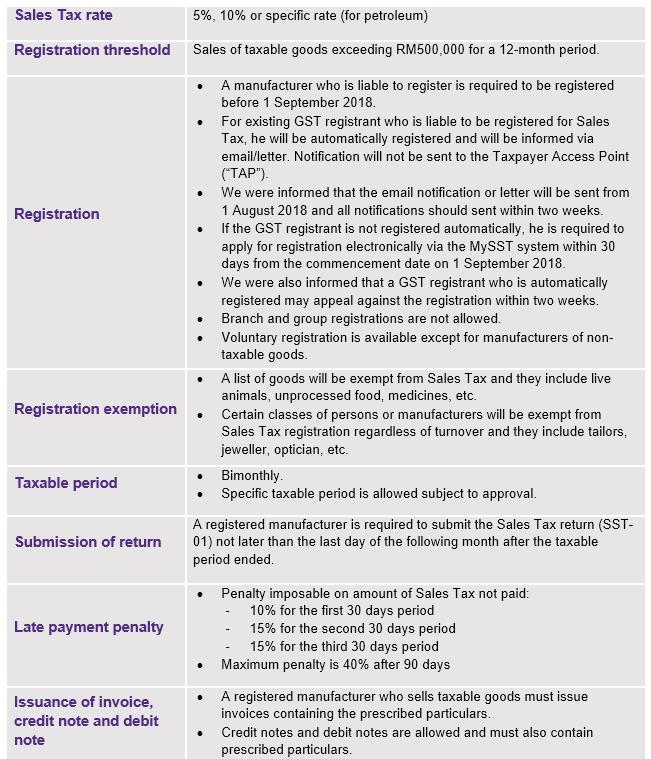

SALES TAX

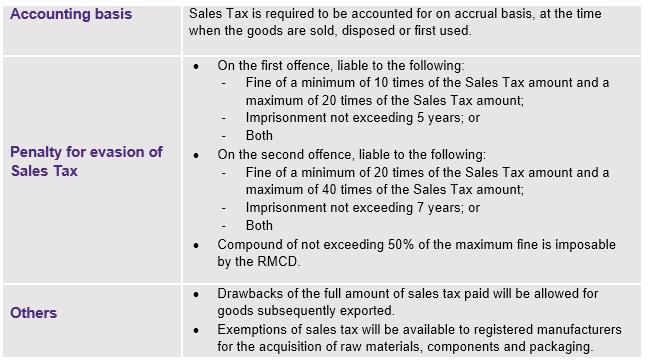

Sales Tax is a single-stage tax charged and levied on taxable goods manufactured and sold in Malaysia by a taxable person as well as taxable goods imported into Malaysia. The activity constituting manufacturing will be defined.

SERVICE TAX

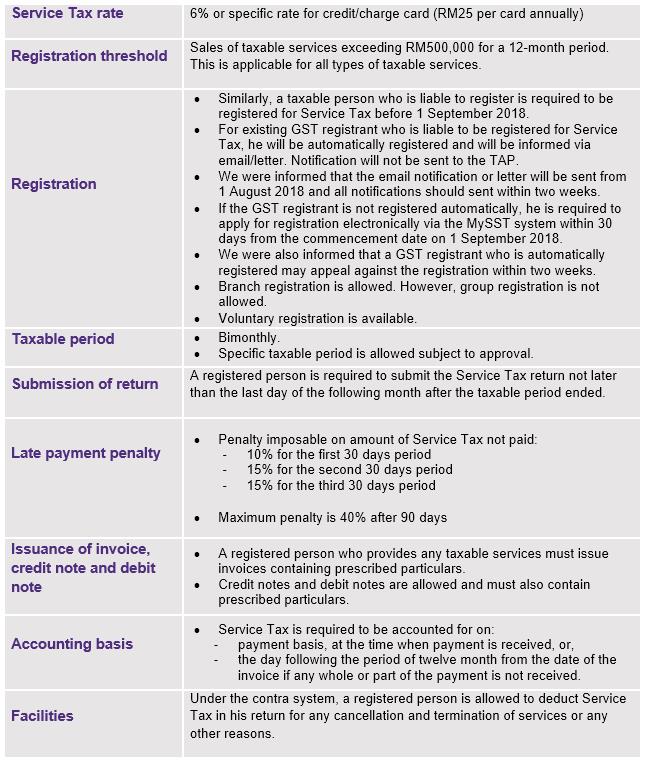

Similarly, Service Tax is a single-stage tax. Service tax is charged on the provision of taxable services made in the course or furtherance of any business by a taxable person in Malaysia.

Service Tax is not applicable to imported services and exported services.

Impact on GST

- There are guidance provided for the transition from GST to SST.

- Input tax from the GST era is claimable within 120 days after the effective date of SST.

- Deregistration of GST is not required. A GST registered person will automatically ceased to be a GST registered person when the Goods and Services Tax Act 2014 is repealed.

- A GST registered person is required to account for output tax at the standard rate of 0% for goods held on hand before the effective date of SST.

- Audits for closure of GST will still be carried out after 1 September 2018.

Please do not hesitate to contact us should you wish to discuss any matters relating to SST or GST.